01Time Machine

See what hasn't happened yet

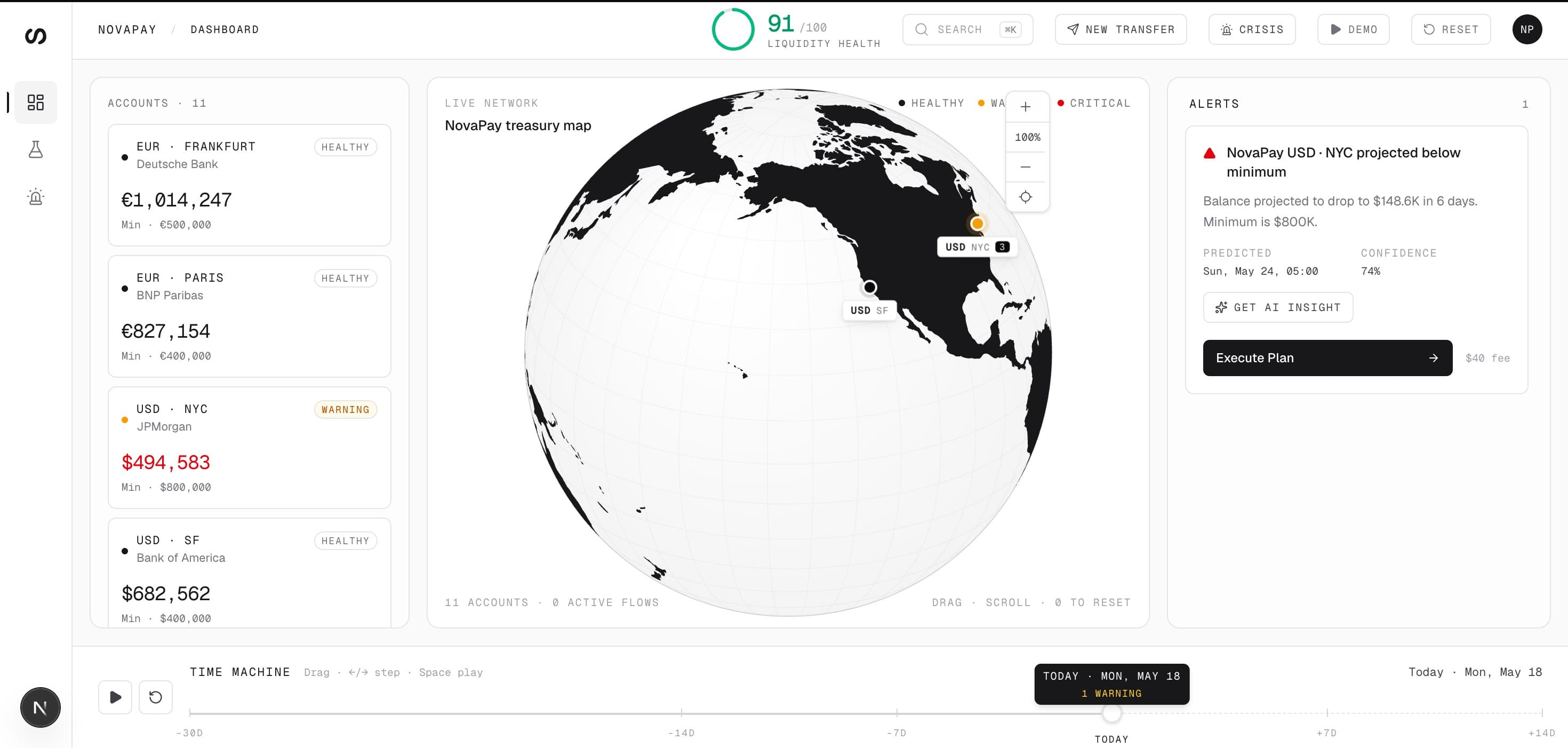

Drag Time Machine. Every account balance, every status colour, every alert recomputes from real ML predictions fourteen days ahead. USD-NYC is fine today, $150K below minimum on day five — you watch it happen.